If you’ve ever tried to figure out how to fund your business, you already know it can feel like walking through a maze. There are loans, grants, investors, and government portals, and every option seems to come with a pile of conditions and fine print. I assure you, “You’re not alone in feeling that way.”

This guide is meant to help you get through the noise. Whether you’re a startup trying to get off the ground or an established small business looking to grow, we’ll walk you through every major funding option available in Australia, what you actually need to qualify, and how to avoid the mistakes that cost business owners time and money every year.

By the end of this guide, you’ll know exactly where to start and who to call when you need expert help.

If you are thinking to get help, ISM Accountants is here to help you.

What Are Small Business Funding Options in Australia?

Business funding is money that you can get to establish, run, or develop your business. It’s the money that lets you hire people, buy equipment, keep track of your cash flow, or move into new markets.

Small and medium-sized businesses (SMEs) in Australia can get money from a wide range of sources, including traditional bank loans, government subsidies, private investors, and new fintech solutions. The best choice for you will depend on your business’s stage, your finances, and what you need the money for.

For instance, a tradie who wants to establish their own business might get a small secured loan to buy a work vehicle. A tech startup, on the other hand, may seek R&D funding or venture capital to support the development of their product. There isn’t one “best” option; you have to pick the one that works best for you.

Recommended Read: How to Manage Business Debt and Improve Financial Health?

Types of Small Business Funding in Australia (Full Breakdown)

Let me explain to you the main types of funding that small businesses in Australia can get. Each one has its own benefits and cons, works in different scenarios, and has its own eligibility requirements.

Business Loans (Secured & Unsecured)

In Australia, the most popular way for small businesses to get money is through business loans. You borrow a certain amount from a lender and pay it back over time, with interest.

For a secured loan, you have to put up something of value as collateral. This may be a car, a piece of property, or a piece of equipment. Interest rates are usually cheaper because the lender has security. Unsecured loans, on the other hand, don’t need collateral, which makes them easier to get, but lenders make up for the risk by charging higher interest rates and requiring more income.

You can apply for business loans through major Australian banks like ANZ, NAB, Commonwealth Bank, and Westpac or through specialist business lenders and fintech platforms.

- Pros: Quick access to capital, flexible use of funds, builds business credit history.

- Cons: Must be repaid with interest; lenders assess your credit score and revenue; collateral may be required for larger amounts.

Recommended Read: Perth Small Business Tax Tips

Government Grants (Free Funding Options)

Grants are one of the most appealing options because, unlike loans, you don’t have to pay them back. The Australian government at federal, state, and local levels regularly offers grants to support small businesses in specific sectors, regions, or activities.

Common examples include R&D grants, export market development grants, and grants for regional businesses or Indigenous entrepreneurs.

The catch? Grants are highly competitive and come with strict eligibility criteria. They usually require you to spend on an approved activity first and then claim reimbursement or to meet very specific conditions before funding is released.

- Pros: No repayment required, can be substantial amounts, and supports specific growth activities.

- Cons: Highly competitive, time-consuming to apply, limited to approved purposes.

Line of Credit & Overdrafts

A business line of credit or overdraft gives you access to a set pool of funds that you can draw from as needed. You only pay interest on what you use, which makes it a smart tool for managing cash flow gaps or unexpected expenses.

This option suits businesses that have irregular income cycles, like seasonal businesses or those waiting for large invoice payments.

- Pros: Flexible drawdown, interest only on what you use, reusable facility.

- Cons: Can be tempting to over-rely on; fees and interest still apply.

Invoice Financing & Equipment Finance

If your business regularly issues invoices and has cash tied up waiting for clients to pay, invoice financing lets you unlock that cash quickly. A lender advances you a percentage of your outstanding invoices, often 70–90%, and you repay once your clients settle up.

Equipment finance is used specifically to buy or lease business equipment like machinery, vehicles, or technology. The equipment itself often serves as the collateral, making it easier to qualify for than unsecured loans.

- Pros: Solves real cash flow problems, tied to your actual business activity.

- Cons: Fees and charges, client payment behaviour affects your cash position.

Recommended Read: Australian Tax Laws For Small Businesses

Investors (Angel Investors & Venture Capital)

If you’re building a high-growth business and willing to give up a share of ownership in exchange for capital, equity funding might be the path for you.

Angel investors are typically wealthy individuals who invest their own money in early-stage businesses. They often bring industry experience and networks in addition to cash.

Venture capital (VC) firms invest larger amounts but usually want a meaningful equity stake and a clear pathway to a significant return, often through a sale or public listing.

- Pros: Large amounts of capital available, bring expertise and networks.

- Cons: You give up part ownership, investors expect fast growth and returns.

Crowdfunding & Peer-to-Peer Lending

These are relatively new but increasingly popular options in Australia.

Crowdfunding platforms like Birchal and VentureCrowd allow businesses to raise capital from a large number of individual contributors either as donations, pre-purchases, or equity investments.

Peer-to-peer (P2P) lending connects businesses directly with individual investors willing to lend money, often at competitive rates and with faster turnaround than traditional banks.

- Pros: Accessible, good for brand awareness, less reliance on traditional lenders.

- Cons: Requires strong marketing effort, may not raise target amounts, and regulatory requirements apply for equity crowdfunding.

Comparison Table: Funding Options at a Glance

A quick look at the different funding options.

Funding Type | Repayable | Speed | Typical Use Case | Risk Level |

Business Loan | Yes | Days–Weeks | Growth, working capital | Medium |

Government Grant | No | Weeks–Months | Specific activities | Low |

Line of Credit | Yes | Fast | Cash flow gaps | Medium |

Invoice Finance | Yes | Very Fast | Unpaid invoices | Low–Medium |

Equipment Finance | Yes | Days | Machinery, vehicles | Low |

Angel/VC Investors | No (equity) | Variable | Startups, scale-ups | High |

Crowdfunding | Varies | Weeks | Product launches | Medium |

P2P Lending | Yes | Fast | Working capital | Medium |

Recommended Read: Bookkeeping Mistakes by Small Businesses

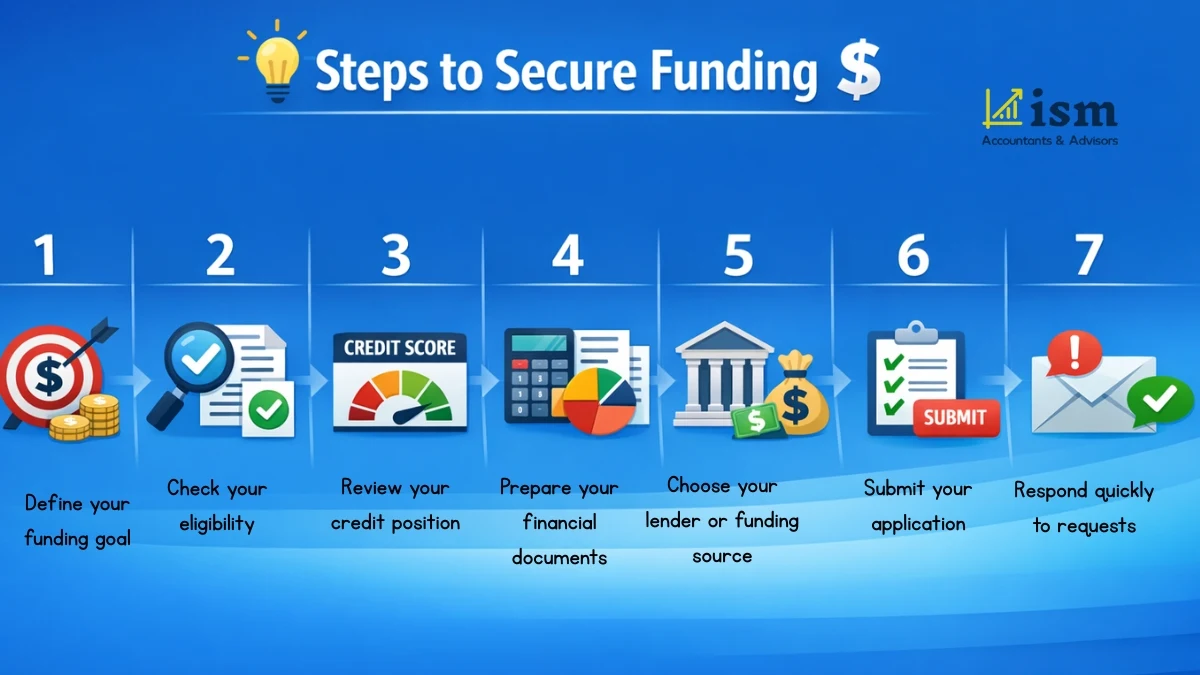

How to Apply for Small Business Funding in Australia (Step-by-Step)

Getting funding isn’t just about finding the right option; it’s about putting your best foot forward when you apply. Here’s how to approach it.

Step 1: Define your funding goal. Be clear about how much you need, what you’ll use it for, and how long you need to repay it.

Step 2: Check your eligibility. Different lenders and grant programs have different criteria. Review the requirements before you spend time preparing an application.

Step 3: Review your credit position. Check your personal and business credit scores. Address any errors or outstanding issues before applying.

Step 4: Prepare your financial documents. This stage is often where applications stall. Get your paperwork organised in advance.

Step 5: Choose your lender or funding source. Compare options; don’t just go with the first lender you find.

Step 6: Submit your application. Follow all instructions carefully. Missing documents or incomplete sections are among the most common reasons for delays.

Step 7: Respond quickly to requests. If the lender requests additional information, turn it around fast. Delays on your end can mean losing your spot in the queue.

Documents You Need Before Applying

Having your documents ready in advance can significantly accelerate the approval process. From my experience, the common documents asked by lenders and grant bodies:

- Last 2–3 years of business financial statements

- Recent business tax returns (lodged with the ATO)

- 3–6 months of business bank statements

- A current business plan (especially for grants and startup loans)

- Cash flow forecasts for the next 12 months

- Government-issued ID (passport or driver’s licence)

- ABN/ACN registration details

- Details of any existing debts or liabilities

Where to Apply (Trusted Platforms & Lenders)

After you set up all the documents. The upcoming question would be “Where to apply?” The options are:

- Major banks: ANZ, NAB, Commonwealth Bank, Westpac ideal for established businesses with strong financials

- Government portals: business.gov.au is the central hub for Australian government grants and programs

- Fintech lenders: Prospa, Moula, Lumi, and OnDeck offer fast, flexible business loans

- State government programs: Each state government runs its own grant and support programs

Need help putting your funding application together? The team at ISM Accountants & Advisors Pty Ltd helps small businesses across Australia prepare financials, cash flow forecasts, and business plans that make lenders and grant bodies take notice. Get in touch today and let’s improve your chances of approval.

Government Grants in Australia (Complete Guide)

Government grants are one of the most searched topics for small business owners and with good reason. Free funding that doesn’t require repayment is understandably appealing. But there are a few things you need to understand before you start applying.

Where to find grants: Start at business.gov.au, which lists federal grants and programs. Your state government website (e.g., Business Victoria, Service NSW, Business Queensland) will list state-specific programs. Don’t overlook local council grants either.

Here are some tips to maximize your chances:

- Read the eligibility criteria carefully. Applying for a grant you don’t qualify for is a waste of time

- Tailor your application to the grant’s stated goals and language

- Provide supporting evidence wherever you can (financials, testimonials, projections)

- Apply early; some grants close as soon as funds are exhausted

- Consider engaging a grants specialist or accountant to review your application

Popular Grant Programs You Should Know

- R&D Tax Incentive: A government program that provides tax offsets for eligible research and development activities. Administered by the ATO and AusIndustry.

- Export Market Development Grant (EMDG): Helps Australian businesses enter and grow in overseas markets by reimbursing eligible export promotion expenses.

- New Enterprise Incentive Scheme (NEIS): Provides mentoring and allowance support for eligible individuals starting a new business.

- State-based COVID and recovery grants: While many of these programs have wound down, new business recovery and resilience grants continue to be offered.

- Industry-specific grants: Agriculture, clean energy, manufacturing, and technology are commonly supported sectors at both federal and state levels.

Recommended Read: Single Touch Payroll for Small Businesses

Who Qualifies for Business Grants?

Eligibility varies significantly by program, but common criteria include:

- Registered ABN (and GST registration in many cases)

- Business must be operating within Australia

- Minimum or maximum revenue thresholds

- Specific industry or activity requirements

- Demonstrated need or alignment with program goals

- Some programs are limited to businesses in regional or rural areas

Fast & Easy Funding Options (For Urgent Needs)

Sometimes you don’t have weeks to wait. Whether it’s an unexpected expense, a cash flow crunch, or an opportunity you need to move on quickly, fast funding options do exist in Australia.

Same-day and 24-hour business loans are offered by many fintech lenders. Platforms like Prospa, Lumi, and OnDeck can assess applications and deposit funds in as little as 24 hours. The trade-off is typically higher interest rates and shorter repayment terms.

Invoice financing can also be accessed quickly; once set up, some platforms settle funds within hours of submitting an invoice.

Business credit cards and overdrafts are another immediate option if you already have them in place.

Be cautious of these when considering fast funding:

- Annual percentage rates (APRs) on short-term loans can be very high; compare the total cost, not just the weekly repayment

- Some lenders charge establishment fees, monthly fees, and early repayment penalties

- Speed is useful, but make sure you’re borrowing what you can actually afford to repay

Eligibility Criteria for Business Funding (What Lenders Check)

Understanding what lenders look for before you apply can save you a lot of time and protect your credit score from unnecessary hard enquiries.

- Credit score: Both your personal and business credit scores matter, especially for unsecured loans. Most mainstream lenders prefer a score above 600, though fintech lenders may work with lower scores if your cash flow is strong.

- Business revenue: Lenders want to see consistent revenue. Many require a minimum monthly turnover, commonly $5,000–$10,000 per month, for small business loans.

- Time in business: Most banks require at least 2 years of trading history. Fintech lenders are often more flexible, with some accepting businesses as young as 6 months.

- Cash flow: Lenders assess whether you can service the debt. Consistent positive cash flow is a strong indicator. If your bank statements show irregular or negative cash flow, address this before applying.

- Existing debt: High levels of existing debt reduce your borrowing capacity. Lenders calculate a debt service coverage ratio. The higher your existing obligations, the less room there is to take on new debt.

- Business plan and forecasts: For larger loans and grants, a credible business plan with realistic financial projections is often essential.

Recommended Read: Business Structure for Small Businesses in Australia

Interest Rates, Fees & Repayment Terms Explained

Borrowing money always has a cost. Understanding how interest rates and fees work helps you compare options properly, not just go for the one with the most attractive-looking headline number.

Interest rates in Australia for business loans vary widely. Bank loans for established businesses might sit between 6% and 12% per annum, while unsecured fintech loans can range from 15% to 40%+ APR depending on your risk profile and loan term.

Key fees to watch for:

- Establishment/origination fees: Charged upfront, often 1–3% of the loan amount

- Monthly account fees: A flat fee charged each month for the life of the loan

- Early repayment fees: Some lenders penalise you for paying off your loan early

- Missed payment fees: Can add up quickly if cash flow becomes tight

Repayment terms range from 3 months (short-term working capital loans) to 10+ years (secured property-backed business loans). Shorter terms mean higher regular repayments but less interest paid overall. Longer terms are easier on cash flow but cost more over time.

Example: A $50,000 unsecured business loan at 18% p.a. over 3 years would cost approximately $15,000–$18,000 in total interest before fees. Always ask for a comparison rate and a full fee schedule before signing.

Funding Mistakes to Avoid (Learn Before You Apply)

These are the mistakes that cost Australian small business owners time, money, and sometimes their credit rating. Learn them now so you don’t repeat them.

- Borrowing the wrong amount. Underestimating your needs leads to going back for more (expensive). Overestimating means you’re paying interest on money you don’t need. Model your cash flow first.

- Ignoring the comparison rate. The advertised interest rate is not the full picture. The comparison rate includes most fees and gives a truer cost of the loan.

- Not reading the loan contract. Early repayment clauses, prepayment penalties, and variation fees are buried in loan documents. Read everything or have your accountant review it.

- Applying for everything at once. Multiple credit applications in a short period create multiple hard enquiries on your credit file, which can lower your score and signal desperation to lenders.

- Applying for grants you don’t qualify for. Wasted effort that could have been spent on a relevant application.

- No business plan or cash flow forecast. Walking into a loan or grant application without supporting documents is one of the most common reasons for rejection.

- Over-borrowing. Taking on more debt than your cash flow can support is the fastest route to financial stress. Borrow what you need, and model the repayments before you commit.

Business Loans vs Grants vs Investors (Which Is Best?)

There’s no one-size-fits-all answer, but this comparison will help you figure out which option suits your situation best.

Feature | Business Loan | Government Grant | Equity Investor |

Repayment required | Yes | No | No (but equity given) |

Speed of access | Days to weeks | Weeks to months | Months |

Amount available | $5K–$500K+ | $5K–$500K+ | $50K–Millions |

Business stage | All stages | Specific criteria | Usually early or growth |

Ownership impact | None | None | You give up a share |

Eligibility complexity | Medium | High | High |

Best for | Working capital, growth | Specific activities | Rapid scale-up |

Scenario 1: A café owner needs $30,000 to refit their kitchen. A secured or unsecured business loan is the most practical option. Grants are unlikely to cover general fitouts; investors won’t be interested in this type of deal.

Scenario 2: Tech startup needs $200,000 for product development. An R&D grant and/or angel investor funding could both be options, depending on eligibility and growth ambitions.

Scenario 3: Retail business needs to cover payroll during a slow season. A line of credit or overdraft is purpose-built for this kind of short-term cash flow gap.

Best Funding Options Based on Your Business Type

You can choose the funds based on your business types.

If you’re a startup (under 2 years old):

Your options may be limited by trading history, but you’re not without choices. Government startup grants, the New Enterprise Incentive Scheme (NEIS), angel investors, and some fintech lenders who accept younger businesses are worth exploring. Having a strong business plan is non-negotiable at this stage.

If you’re an established small business looking to grow:

You’ll likely have the most options available. Bank loans, business credit lines, equipment finance, and government growth grants are all on the table. Your track record works in your favour.

If you’re a business in financial difficulty:

Accessing new funding when you’re already under financial pressure is harder, but not impossible. Invoice financing and short-term loans may help in the short term, but the underlying issue needs addressing. The most crucial initial step is to consult with an accountant or financial advisor.

If you’re in a specific industry:

Agriculture, manufacturing, clean energy, and technology are sectors that attract specific grant programs. Check business.gov.au and your state government portal for industry-focused funding.

Final Thoughts

Funding a small business in Australia is genuinely challenging, but there are more options available than most business owners realise. The key is to understand what you actually need, match that to the right type of funding, and put yourself in the strongest possible position before you apply.

Don’t rush into the first loan you’re approved for. Take the time to compare options, understand the real cost of borrowing, and get your documents in order. The extra effort upfront will save you money and stress in the long run.

And if you’re not sure where to start or want to make sure you’re making the right call, that’s exactly what we’re here for.

ISM Accountants & Advisors Pty Ltd works with small businesses across Australia to navigate funding decisions, prepare financial documents, and structure applications for loans and grants. Whether you’re just starting out or looking to take your next growth step, we can help you approach lenders and grant bodies with confidence.

Get in touch with the ISM team today and let’s find the right funding option for your business.

Frequently Asked Questions

The best option depends on your specific needs. Loans provide quick access to capital but must be repaid with interest. Grants are free but highly competitive and limited to approved purposes. Startups often rely on investors, while established businesses are better placed to use loans or credit lines. The right answer will depend on your business stage, cash flow, and what the money is for.

Yes, unsecured business loans are widely available in Australia. Lenders like Prospa, Moula, and OnDeck offer unsecured options based on your business’s cash flow and revenue rather than physical assets. Keep in mind that interest rates on unsecured loans are typically higher than secured equivalents.

Yes, government grants don’t need to be repaid. However, they’re competitive, come with strict eligibility criteria, and usually require you to spend on approved activities before claiming. Think of them as a reward for doing the right things, rather than a first port of call for general funding needs.

It depends on the type of funding. Fintech lenders can often approve and deposit funds within 24–48 hours. Traditional bank loans usually take 1–4 weeks. Grant applications can take several months, depending on the program and volume of applicants.

Most traditional lenders prefer a credit score above 600, but there’s no universal threshold. Fintech lenders tend to be more flexible, particularly if your business has strong revenue and consistent cash flow. Before applying, check both your personal and business credit scores through Equifax, Illion, or Experian.

Most lenders and grant bodies will require financial statements, business and personal tax returns, bank statements, a business plan, cash flow forecasts, and photo ID. Having these ready before you apply will speed up the process significantly.

It depends on your goals. A loan allows you to retain full ownership of your business but comes with mandatory repayments. An investor provides capital without repayments, but you give up a share of your business and potentially some control. If long-term independence matters to you, lean toward loans. Investors might be a better option if you’re looking for a growth partner and access to more money.

Yes. Startups can access government grants, angel investor funding, venture capital, and some fintech loans designed for early-stage businesses. A well-developed business plan and financial projections will significantly improve your chances across all of these options.