Superannuation isn’t just a legal checkbox—it’s a real commitment to your employees’ financial wellbeing and future security. As an employer in Australia, understanding superannuation for employers is essential—not only to stay compliant but also to build trust and loyalty within your team.

Handling employer super contributions goes beyond simply paying on time. It means knowing key details like superannuation payment deadlines, employee super eligibility, and collecting the right super fund details for employers. Getting these right can save you from costly penalties and build a stronger workplace culture.

Whether you’re a small business owner or managing a growing team across different locations, this guide breaks down everything you need to know about superannuation for employers—from how much you must contribute, when to pay, who qualifies, to how to report your contributions correctly. Staying informed and organised means protecting your business and showing your employees that their future matters to you.

Ready to take the stress out of super? Let’s make it straightforward and manageable.

What Is Superannuation and Why Do Employers Need to Pay It?

Superannuation, commonly known as “super,” is a government-backed retirement savings system in Australia. As part of superannuation for employers, you are responsible for contributing a portion of your eligible employees’ earnings into a super fund. This ensures your staff have financial support when they retire, making it a vital part of their long-term security.

Legal Obligations for Businesses

Employers are required by the Superannuation Guarantee (SG) statute to contribute a minimum portion of an eligible employee’s regular income to a super fund that complies. Currently, the rate stands at 11%. Because late payments might result in penalties and other charges, it’s essential to meet superannuation payment dates. With better business services, understanding your superannuation compliance requirements helps you avoid these costly mistakes.

Employee Super Eligibility

When it comes to superannuation for employers, it’s important to understand exactly who qualifies for contributions. Usually, full-time, part-time, and even some casual employees are entitled to receive employer super contributions. Knowing your employees’ super eligibility helps you stay compliant and ensures no one who should be covered gets left out. Plus, it clears up any confusion about when super payments aren’t required, making your superannuation process smoother and hassle-free.

The Role of Super in Employee Financial Security

Making consistent super contributions demonstrates your dedication to your employees’ futures, even beyond the legal requirements. Because your staff is aware that you are promoting their long-term well-being, it increases morale, encourages loyalty, and creates trust. This procedure includes gathering the appropriate super fund information for employers, guaranteeing that contributions are sent on schedule and to the appropriate location.

Recommended Read: Departing Australia Superannuation Claim

How Much Superannuation Should Employers Contribute?

Understanding exactly how much you need to contribute is a key part of managing superannuation for employers correctly and avoiding compliance issues.

Super Guarantee Rate Explained

The Super Guarantee (SG) rate will rise to 12% on July 1, 2025. This implies that, as an employer, you must finance an employee’s designated super fund with 12% of their regular time wages. To meet your superannuation compliance needs and stay out of trouble, you must keep an eye on this fluctuating rate.

Earnings Included in Calculations

Knowing which earnings go toward the SG is crucial when figuring out super contributions. These consist of:

- Base pay or earnings

- Commissions received

- Change loadings

- Some allowances

It’s important to keep in mind, though, that overtime compensation is typically not included in these computations and does not go toward your employer’s super contributions.

Common Mistakes in Contribution Calculations

Many employers trip up in this area by:

- Misclassifying employees, which can lead to incorrect SG payments

- Excluding certain allowances that should be factored into calculations

- Failing to update contributions when the SG rate changes, risking non-compliance

Regularly reviewing your payroll and keeping up with the latest laws is key when managing superannuation for employers. Avoiding common mistakes in super calculations doesn’t just keep your business on the right side of compliance—it also shows your employees you care by making sure their super is handled properly and on time. Staying proactive helps build trust and peace of mind for everyone involved.

Recommended Read: Departing Australia Superannuation Payment (DASP)

When Are Super Payments Due and How Frequently Must They Be Made?

As an employer, staying on top of your superannuation payment deadlines is vital to keep your business compliant and avoid unnecessary penalties.

Standard Payment Schedules

Super contributions need to be paid at least quarterly. Here are the key deadlines you need to remember for superannuation for employers:

- For the period 1 July – 30 September, contributions are due by 28 October

- For 1 October – 31 December, contributions are due by 28 January

- For 1 January – 31 March, contributions are due by 28 April

- For 1 April – 30 June, contributions are due by 28 July

Meeting these deadlines is part of the superannuation compliance requirements and helps you avoid costly fines and additional charges.

Recommended Read: Tax Filing Deadline in Australia

Risks of Late Payment and Associated Penalties

If super contributions are paid late, the Australian Taxation Office (ATO) may impose the Superannuation Guarantee Charge (SGC). This charge includes:

- The unpaid super amount you owe to your employees

- Interest on the unpaid amount

- An administration fee

One important point to keep in mind is that late super payments are not tax-deductible, which can impact your business finances. Therefore, making sure your employer’s super payments are paid on time involves more than simply compliance; it also involves prudent cash flow management with improved taxation services.

Importance of Keeping Accurate Records

For employers, maintaining thorough and accurate records is an essential component of superannuation. It’s not just about ticking boxes—clear records build transparency with your employees and make tax compliance checks or ATO audits much easier. Staying on top of your superannuation payment deadlines with well-maintained records gives you peace of mind and safeguards your business reputation.

Who Is Entitled to Super Contributions From an Employer?

Understanding employee super eligibility is essential for employers to meet their superannuation compliance requirements and avoid any costly mistakes.

Eligibility Criteria Based on Employment Type

Generally, as an employer, you are required to make employer super contributions for employees who:

- Are older than eighteen and make more than $450 a month?

- Are you under 18 but work more than 30 hours per week?

Knowing these thresholds helps you determine who should be included in your super payment process and keeps you aligned with Australian superannuation laws.

Casual employees who meet the above criteria are entitled to super contributions just like permanent staff. When it comes to contractors, it’s a bit more nuanced.

Situations Where Super Contributions May Not Be Required

There are specific cases where super contributions are not mandatory, such as:

- Non-resident employees who work entirely outside Australia

- Employees engaged in domestic or private work for 30 hours or less per week

Knowing these exceptions is key when managing superannuation for employers—it helps you avoid making unnecessary payments. But to stay safe and compliant, it’s always a good idea to double-check and make sure you’re meeting your obligations without accidentally missing anything.

Need help navigating employee super eligibility and ensuring you meet all super fund details for employers? At ISM Accountants, our experts are here to guide you through your superannuation obligations with ease.

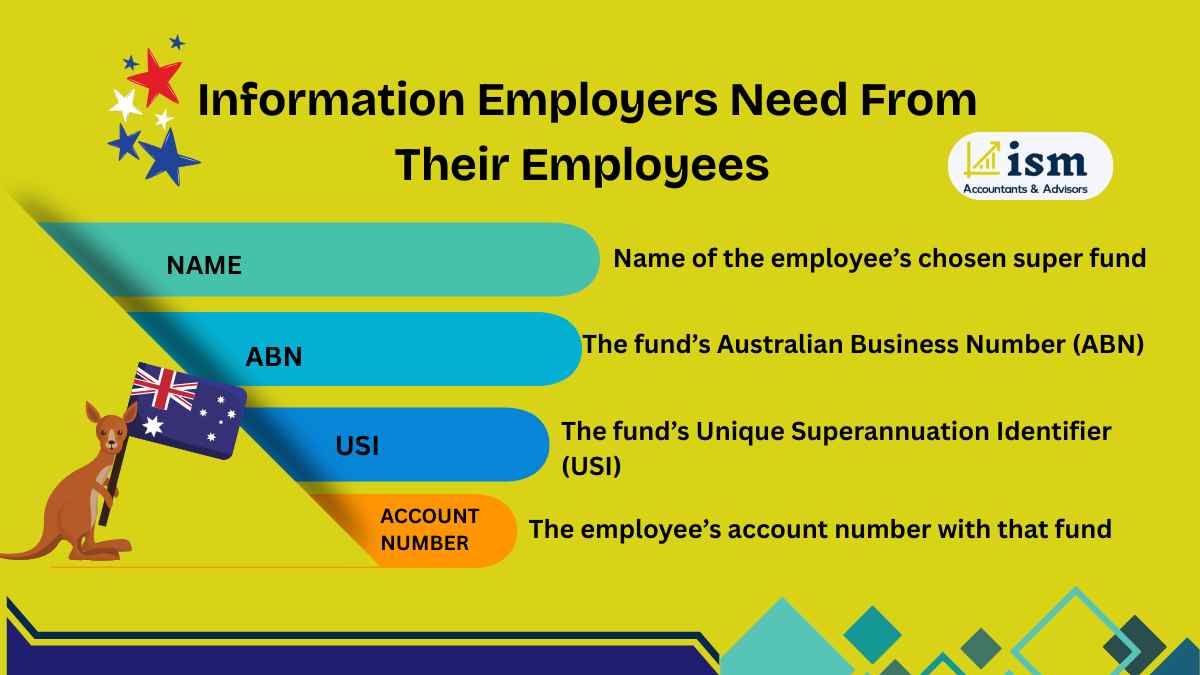

What Information Do Employers Need From Their Employees?

To stay on top of your superannuation compliance requirements, gathering accurate super fund details for employers is absolutely essential. Here’s what you need from each employee to ensure smooth and timely superannuation for employers payments:

Required Super Fund Details

When an employee nominates their super fund, employers must collect:

- The name of the employee’s chosen super fund

- The fund’s Australian Business Number (ABN)

- The fund’s Unique Superannuation Identifier (USI)

- The employee’s account number with that fund

Having the right superannuation for employers information upfront ensures your employer super contributions reach the correct super fund without delays or confusion. This helps keep your payments smooth and your employees happy.

What to Do if No Fund Is Nominated?

Sometimes employees don’t nominate a fund. In those cases, employers are required to:

- Request the employee’s stapled super fund details from the Australian Taxation Office (ATO)

- If there’s no stapled fund, contribute to the employer’s default MySuper fund

This procedure keeps your company in compliance with superannuation payment dates and guarantees that all employees continue to receive their due superannuation.

Employer Steps for Default Fund Selection

If you need to use a default fund, it’s important to follow these steps:

- Choose a MySuper-compliant fund that meets government standards

- Giving your staff members a Superannuation Standard Choice Form allows them to designate a fund if they so choose.

- Keep employees informed about the details of the default fund you’ve selected

By being transparent and organised about super fund details, employers can build trust and make sure they meet all their super obligations efficiently.

How Can Employers Process and Report Super Contributions?

Managing superannuation for employers might seem daunting, but with the right systems and knowledge, it can be straightforward and stress-free.

Employers can use:

- SuperStream-compliant software

- The ATO’s Small Business Superannuation Clearing House

Modern payroll management services can automate super calculations and payments, ensuring timely and accurate contributions.

To Report Obligations Through Government Portals, Employers must:

- Report super contributions via Single Touch Payroll (STP)

- Keep records for five years

What Happens if an Employer Doesn’t Comply With Super Rules?

Failing to meet your superannuation obligations can have detrimental effects on your company. Here’s what you need to know:

- The Superannuation Guarantee Charge (SGC), which consists of unpaid super, interest, and administration fees, might be assessed to you.

- Penalties apply if you don’t lodge SGC statements on time.

- The Australian Taxation Office (ATO) can audit and investigate your business for non-compliance.

- Not paying super on time can damage your reputation and reduce employee trust.

- Regularly review your payroll and super payment processes to stay on track.

- Keep yourself updated on changes to superannuation laws and regulations.

- Seek a professional tax consultant if you’re unsure about your super obligations.

What Changes Are Coming to Superannuation Requirements?

Keeping up with updates in superannuation for employers is crucial to stay compliant and avoid surprises. Here’s what’s on the horizon:

- From July 1, 2026, employers will need to pay super contributions at the same time as wages—this is called “payday super.”

- This change is designed to reduce unpaid super and help employees build their retirement savings faster.

- Employers should be proactive in updating payroll management services and processes to handle these simultaneous payments.

- Early preparation will make the transition smoother and help avoid penalties or compliance issues down the track.

How Can Small and Medium Businesses Stay Super Compliant?

For many small and medium businesses, managing superannuation for employers might feel overwhelming. But staying compliant doesn’t have to be complicated. Here’s a simple checklist to keep you on the right path:

- Confirm which employees are eligible for super contributions.

- Work out the correct amount to contribute, based on the current rules.

- Make sure you pay superannuation on time to avoid any fines.

- Keep thorough records of all super payments and transactions.

- Use systems that meet SuperStream standards for smooth processing.

Helpful tools include:

- Payroll software that automatically calculates and schedules super payments.

- The Australian Tax Office’s Small Business Superannuation Clearing House, which simplifies contributions for smaller businesses.

If you’re ever unsure about your super responsibilities or have tricky cases to handle, don’t hesitate to get advice from an accountant or superannuation expert. It’s a smart way to avoid mistakes and stay compliant.

Recommended Read: Understanding Australian Tax Laws for Small Businesses – ISM Accountants

Why Should Employers Work With a Trusted Accountant for Superannuation?

Handling superannuation for employers can be tricky, and getting it wrong can cost you. Here’s why having a trusted accountant on your side makes all the difference:

- They take the guesswork out of employer super contributions, making sure you get it right every time.

- Stay ahead of changes in superannuation laws without lifting a finger.

- Avoid penalties and compliance headaches with expert guidance.

- Streamline your super payment process so you can focus on growing your business.

- Gain peace of mind knowing your super obligations are in safe hands.

Want to make it super simple? Let a trusted accountant manage it for you.

Conclusion

Employers should understand superannuation because it supports their team’s financial future and fosters a trustworthy work environment, not only to satisfy legal requirements. If you understand your duties, keep accurate records, and seek professional advice when needed, staying compliant and avoiding costly errors is easy.

If you want to make managing super simple and stress-free, contact ISM Accountants for reliable superannuation support tailored to your business needs.

FAQs

As of July 1, 2025, the Super Guarantee rate is 12% of an employee’s ordinary time earnings.

At least quarterly, with specific due dates: 28 October, 28 January, 28 April, and 28 July.

Employers may incur the Superannuation Guarantee Charge, which includes the unpaid amount, interest, and an administration fee.

Most employees are, including casuals and some contractors, depending on their work arrangements.

Employers should request the employee’s stapled super fund from the ATO or contribute to the default MySuper fund.

A default fund is where contributions are made if an employee doesn’t choose a fund. Employers should select a MySuper-compliant fund.