Most small business owners know their cash balance, but that is not the same as knowing their financial position. When you rely on a rough bank balance to make decisions, you expose yourself to tax surprises, cash shortfalls, and compliance breaches that compound over time. The businesses that scale without drama are the ones that treat bookkeeping as a live operational system, not a year-end clean-up exercise.

This guide covers the exact practices that keep Australian small businesses compliant, audit-ready, and genuinely profitable.

Quick Review

- Keep personal and business finances separate.

- Use cloud accounting software such as Xero, MYOB, or QuickBooks.

- Record income and expenses on a regular basis.

- Digitise and store receipts for ATO compliance.

- Reconcile bank accounts every month.

- Monitor cash flow to avoid financial surprises.

- Set aside funds for GST, tax, and superannuation obligations.

- Review financial reports regularly to track business performance.

- Avoid common bookkeeping mistakes that can lead to compliance issues.

- Consider professional bookkeeping support as your business grows.

Why Robust Bookkeeping Matters for Australian Businesses?

Clean books do three things that directly affect your bottom line.

- Real-time cash flow visibility. When your records are current, you can see your cash runway weeks ahead, not after the crisis hits. You move from reacting to shortfalls to planning around them.

- Lower accounting fees. Accountants charge for the time spent reconstructing your records. Clean, reconciled books handed over at year-end significantly reduce that bill.

- Audit defense. The ATO uses sophisticated data-matching to flag inconsistencies. If you are ever selected for review, you can rely on a transparent, verifiable transaction history that provides your strongest protection.

Recommended Read: Can I Do Bookkeeping Without Being a BAS Agent?

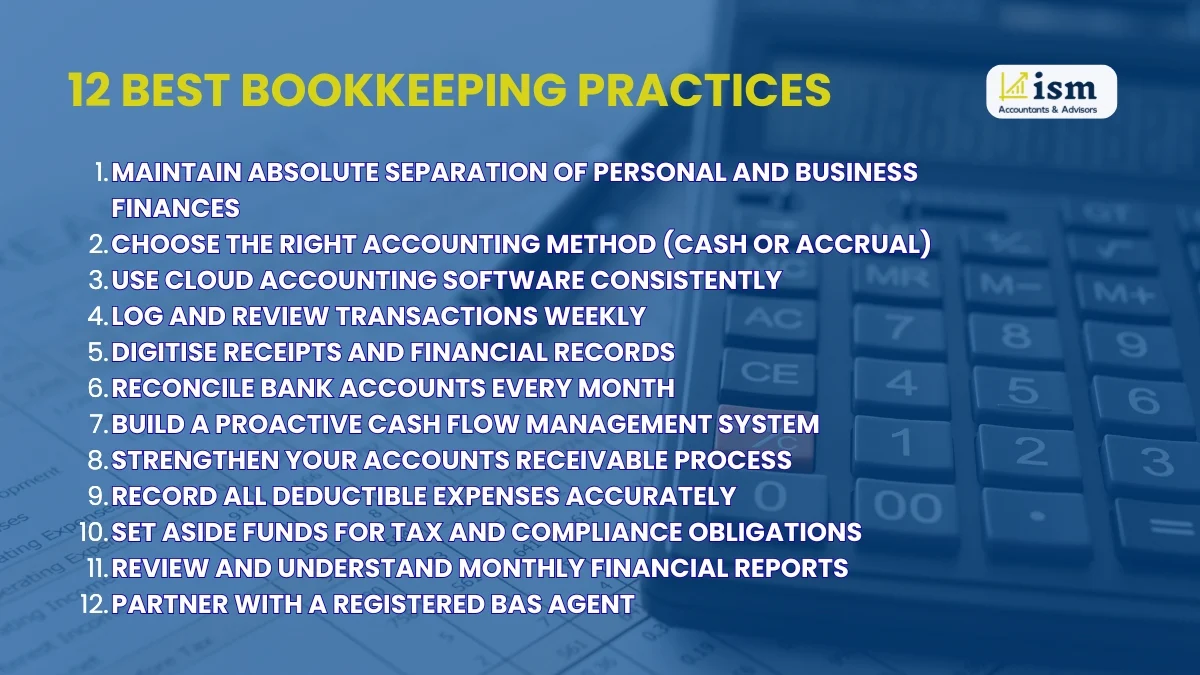

12 Best Bookkeeping Practices Every Australian Business Must Follow

Good bookkeeping habits help Australian businesses maintain compliance, improve cash flow, and make smarter financial decisions throughout the year.

- Maintain absolute separation of personal and business finances

- Choose the right accounting method (cash or accrual)

- Use cloud accounting software consistently

- Log and review transactions weekly

- Digitise receipts and financial records

- Reconcile bank accounts every month

- Build a proactive cash flow management system

- Strengthen your accounts receivable process

- Record all deductible expenses accurately

- Set aside funds for tax and compliance obligations

- Review and understand monthly financial reports

- Partner with a registered BAS agent

1. Maintain Absolute Separation of Personal and Business Finances

Commingling personal and business funds is a common and damaging mistake small business owners make. It obscures your actual profit margins, destroys your audit trail, and causes lost deductions at tax time.

Open a dedicated business transaction account and a separate business credit facility from day one. Treat every personal transfer as a formal drawing or loan, and record it accordingly.

2. Choose the Right Accounting Method: Cash or Accrual

Cash-basis records income when received and expenses when paid. It is simpler and better suited to sole traders and service businesses with straightforward cash cycles.

The accrual basis records income when earned and expenses when incurred, regardless of when money moves. It gives a more accurate picture for businesses with long fulfillment cycles, outstanding invoices, or inventory.

If you are unsure which method suits your structure, it is worth considering as part of a broader tax planning strategy since the method you choose affects how income and deductions land across financial years.

3. Use Cloud Accounting Software and Use It Properly

Choosing the right platform matters less than using your chosen platform consistently. For Australian businesses, the three dominant options are Xero, MYOB, and QuickBooks Online each suited to different business sizes and workflows.

The single most impactful feature in any of these platforms is automated bank feeds. Connecting your bank account to your accounting software eliminates manual data entry, reduces errors, and ensures your ledger stays current in near real-time.

Recommended Read: Xero vs Myob vs Quickbooks

4. Log Transactions on a Weekly Cadence

Letting transactions pile up until the end of a quarter is how errors compound. Invoices go missing. Payment dates blur. Expense categories get misapplied.

Block 30–60 minutes each week to review transactions, categorise any uncoded items, and confirm your bank feed is reconciling cleanly. This weekly discipline is what keeps annual compliance fast and inexpensive.

5. Digitise Every Receipt to Meet the ATO 5-Year Record-Keeping Rule

The ATO requires businesses to retain financial records for a minimum of five years. Thermal paper receipts fade, physical files get lost, and paper does not survive a flood or fire.

Tools like Dext or Hubdoc photograph and extract invoice metadata via OCR the moment you receive a receipt. For a full breakdown of what records must be kept, in what format, and for how long,

Read our dedicated guide on record keeping for Australian businesses.

6. Reconcile Your Bank Accounts Every Month Without Exception

Monthly bank reconciliation means systematically matching every transaction in your accounting software against your actual bank statement. It catches merchant errors, duplicate charges, unauthorised transactions, and banking omissions before they compound.

This process should be completed and locked before the next month begins not left as an open task to revisit later.

7. Build a Proactive Cash Flow Management System

Cash flow management that reacts to situations means finding out you cannot cover payroll on a Thursday afternoon. Proactive management means you are already aware of issues three weeks in advance. The structure is straightforward:

- Every 7 days: Review current cash on hand alongside aging accounts receivable and upcoming accounts payable.

- End of month: Run a formal profit & loss statement and cash flow statement to identify where costs are creeping up unexpectedly.

- Forward-looking: Before touching operational profit, calculate your outstanding GST liability, PAYG withholding, and superannuation owing. These are liabilities sitting in your account, not income.

8. Tighten Your Accounts Receivable Workflow

Late payments are a cash flow problem dressed as a revenue problem. Set clear payment terms on every invoice 7 or 14 days is standard for most service businesses. Offer online payment options to remove friction, and use your accounting software’s automated reminder sequences to follow up overdue invoices without the awkward phone calls.

If invoices regularly go unpaid beyond your terms, the problem is usually a combination of unclear payment terms and no escalation process.

Our guide on handling late payments and bad debt covers both.

9. Record All Deductible Expenses Accurately

The ATO allows a broad range of deductions for legitimately incurred business expenses but only if they are properly documented. This means categorising expenses correctly in your accounting software, not lumping them into a “miscellaneous” line.

Home office usage requires a usage log. Motor vehicle expenses require either a logbook (12 weeks minimum) or the cents-per-kilometer method. Equipment, subscriptions, and professional development costs all have specific rules.

Our guide to common tax deductions for small businesses covers each category with the documentation the ATO expects.

10. Set Aside Tax and Compliance Reserves

A practical guideline: every time revenue hits your account, move a defined percentage into a separate reserve account for GST, income tax, and superannuation. Treat these allocations as non-negotiable liabilities because they are.

Critical 2026 update Payday Super: From 1 July 2026, employers must remit superannuation contributions alongside every individual pay run rather than quarterly. The ATO monitors compliance in real-time. Businesses still running quarterly super cycles risk automatic penalties and daily interest charges.

11. Read Your Monthly Financial Reports Don't Just Run Them

The three reports every business owner should review monthly:

- Profit & Loss (P&L): Revenue versus expenses over a period. Tells you whether the business is performing.

- Balance Sheet: Assets, liabilities, and equity at a point in time. Tells you whether the business is healthy.

- Cash Flow Statement: Actual cash movement. Tells you whether the business is liquid.

Running these reports is the easy part. The value is in reading them spotting trends, questioning anomalies, and acting early.

12. Partner with a Registered BAS Agent

BAS agents are registered professionals who prepare and lodge business activity statements, advise on GST treatment, and can represent you with the ATO. As your business grows, so does the compliance burden around BAS, STP payroll, and superannuation reporting.

Top Bookkeeping Software in Australia

Platform | Best For | Key Strengths | ATO Compliance |

Xero | Modern SMBs | 1,000+ integrations; seamless receipt capture | Full STP Phase 2 |

MYOB | Scaling businesses with inventory | Localised Australian supplier networks | Full STP Phase 2 |

QuickBooks | Contractors and micro-businesses | Simplified expense tagging | Integrated STP payroll |

Common Bookkeeping Mistakes and Their Real Costs

Mistake | Compliance Risk | Financial Impact |

Commingling funds | Triggers ATO audit scrutiny | Lost deductions; inflated accounting fees |

Losing receipts | Breach of ATO 5-year record-keeping rule | Disallowed deductions; back-taxes |

Delayed reconciliations | Undetected duplicates and fraud | Sudden working capital shortfalls |

Misclassifying contractors | Wrong payroll treatment under ATO worker rules | Liability for back-paid super contributions |

The Small Business Bookkeeping Checklist

Daily: Log sales and snap receipt images via mobile capture.

Weekly: Review bank feed transactions; authorise vendor payables.

Monthly: Reconcile all accounts; run P&L and cash flow reports; lock prior-month records.

Quarterly: Finalise BAS; clear outstanding GST liabilities; review tax reserve balances.

When to Outsource: Signs You Need a Certified Bookkeeper

The tipping point is usually one of three things: your transaction volume has grown past what you can manage in a few hours a week, payroll has become complex enough that errors are likely, or you are spending evenings troubleshooting accounting software instead of running your business.

If you are hitting any of these, our post on who needs bookkeeping services in Australia walks through the indicators in detail and what a professional engagement typically looks like.

How ISM Accountants Supports Your Business?

ISM Accountants & Advisors is a Perth-based firm providing registered BAS agent services, Xero provisioning and training, automated spend management setups, and complete STP Phase 2 payroll compliance management.

Whether you need a bookkeeping system built from scratch or ongoing monthly support, the team works directly with your existing software environment to keep your books clean, compliant, and decision-ready year-round.

See the bookkeeping services ISM offers or get in touch to discuss your situation.

Final Thought

Strong bookkeeping helps you stay compliant, manage cash flow, and make better business decisions. By keeping accurate records and managing your finances, you can avoid costly mistakes and support long-term growth. If bookkeeping is becoming difficult to manage, professional support can help keep your business organised, compliant, and ready for success.

Contact ISM Accountants today to discuss your bookkeeping needs and discover how professional support can save time, reduce stress, and help your business grow.

FAQs

The core framework is to separate personal and business finances, choose the right accounting method, use cloud software with automated bank feeds, log transactions weekly, digitise all receipts, reconcile monthly, and stay current on BAS and superannuation obligations.

The ATO requires a minimum of five years from the date of lodgement of the relevant return. Digital storage is the most reliable method for meeting this requirement.

Bookkeeping is the systematic recording and categorisation of daily transactions. Accounting uses that data for higher-level analysis, tax planning, and strategic financial advice. Clean bookkeeping makes accounting significantly faster and less expensive.

Under Payday Super regulations effective July 2026, late contributions attract automatic penalties and daily interest charges. The ATO monitors this in real-time, removing the quarterly buffer businesses previously relied on. Persistent non-compliance can escalate to director penalty notices.