Year End Tax Planning for Small Businesses in Australia helps you pay less tax, get the most deductions, and have more cash on hand before 30 June. Planning early lets you claim all the expenses you can, use government incentives, and follow ATO rules.

It lowers the amount of tax you have to pay by including deductions for rent, insurance, software, professional fees, and other business costs. Paying some expenses early and writing off old stock or unpaid debts can also reduce your tax.

Planning this way also helps with cash flow, giving you money to reinvest or grow your business in the new financial year. It keeps your records in order too, which lowers the chance of penalties or ATO audits.

In short, good year-end tax planning makes your business’s finances stronger, keeps you following the rules, and gets your small business ready for a successful year ahead.

What Is EOFY (End of Financial Year) Tax Planning?

EOFY tax planning is the process of organising business finances and transactions before 30 June to reduce tax obligations, claim all eligible deductions, and take advantage of government incentives.

Why it matters for small businesses in Australia:

- Ensures compliance with ATO requirements

- Helps in maximising tax deductions and offsets

- Supports better cash flow management

Key deadlines to keep in mind:

- 30 June – last day to claim certain deductions and prepayments

- BAS lodgement dates – varies depending on quarterly or monthly reporting

- 31 October – standard tax return lodgement deadline

Core Year‑End Tax Planning Strategies For Small Businesses

Effective year-end tax planning ensures your small business reduces tax, maximises deductions, and stays compliant with the ATO before 30 June. By applying these core strategies, you can improve cash flow, lower taxable income, and prepare for the new financial year.

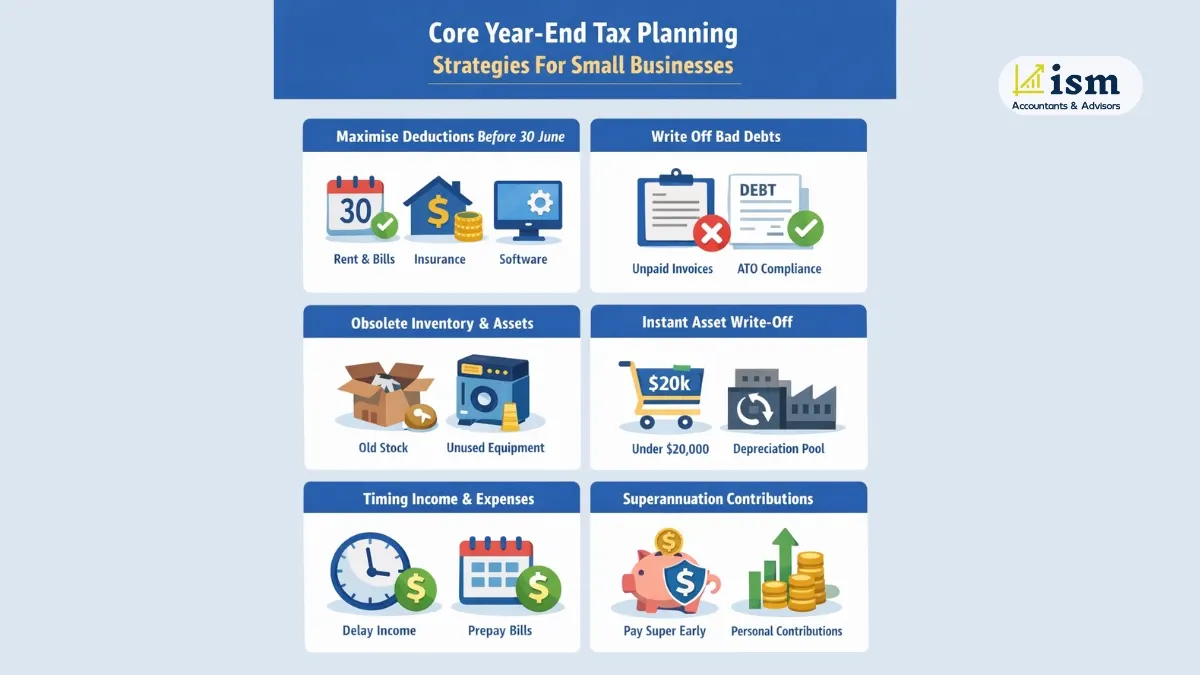

1. Maximise Deductions Before 30 June

One of the easiest ways to pay less tax is to make sure you claim all the business expenses you can before 30 June. Doing this lowers your taxable income and can give your business more cash to use in the new financial year.

Some expenses you can pay early are:

- Rent or lease payments

- Insurance premiums

- Software subscriptions

- Marketing and advertising costs

Paying for these things early moves the deductions into this financial year, so your business saves on tax now instead of later. ISM Accountants, best accountant in Perth, Australia can help you with your tax planning strategy.

Writing Off Bad Debts

If a customer doesn’t pay what they owe, you can write off that debt as a tax deduction. This helps reduce your taxable income for this year.

To claim it, the debt must:

- Have been counted as income before

- Be officially written off before 30 June

- Include any GST adjustments needed

Doing this properly keeps your records correct and makes sure your business follows ATO rules.

Obsolete Inventory & Assets

Take a look at your stock and equipment to see if you have:

- Damaged, old, or slow-selling stock

- Old or unused equipment

Throwing out or scrapping these items before EOFY can give you extra deductions.

Consumables

Things you use up quickly, like consumables or spare parts you’ll use within three months of EOFY, can be deducted straight away instead of being added to closing stock.

Recommended Read: Tax Filing Deadlines in Australia

2. Instant Asset Write-Off & Depreciation Rules

The instant asset write-off allows small businesses to deduct the full cost of eligible assets in the year they are first used.

Eligibility for 2024–25

- Assets must cost less than $20,000

- Small businesses must have a turnover under $10 million

- Assets must be first used or installed by 30 June 2025

Higher-Cost Assets

- Assets costing $20,000 or more go into a simplified depreciation pool

- Deduction rates: 15% in the first year and 30% in subsequent years

Note: The write-off threshold is scheduled to revert to $1,000 from 1 July 2025 unless legislation extends it.

Table: Asset Tax Treatment (2024‑25 vs Future)

Asset Type | Write-Off 2024‑25 | Depreciation Rule |

Equipment <$20,000 | Full deduction | Immediate |

Larger assets | Pool depreciation | 15% first year, 30% next year |

Recommended Read: Business Structure for Small Business in Australia

3. Timing Income & Expenses

The timing of when you get paid and when you pay your bills can actually help you save on tax.

Here’s how:

- You can hold off on sending some invoices until after 30 June, so the income counts next year instead

- Pay regular bills early, like rent, insurance, or subscriptions, to bring deductions into this year

- Just don’t try any tricky schemes — the ATO might notice and check your records

4. Superannuation Contributions

Superannuation is one of the best ways to save on tax, whether you run a business or are an employee.

Timing Matters

- You can only claim a deduction once the fund actually receives the money

- Paying employee super before 30 June means you can include it in this year’s deductions

Personal Contributions

- You can also put in extra voluntary contributions to reduce your personal taxable income

- The concessional cap is $27,500 for 2023–24 and goes up to $30,000 from 1 July 2024

Catch-Up Contributions

If your total super is under $500,000, you can use any unused cap from the last five years to make bigger contributions and claim more deductions

Recommended Read: Departing Australia Superannuation Claim

5. Trading Stock & Inventory Tax Planning

Managing your trading stock properly can help reduce your tax and avoid ATO penalties. Knowing the value and condition of your stock ensures your business claims all the deductions it is entitled to.

Key recommendations:

- Conduct a stocktake before 30 June

- Value stock using cost, market, or replacement methods

- Write off obsolete, damaged, or slow-moving stock to claim deductions

Proper stock management not only lowers taxable income but also keeps your records accurate and compliant.

Recommended Read: Can ATO Track ABN Income?

6. Write Off Bad Debts

Writing off bad debts lets your business remove unrecoverable income from your taxable income, reducing your tax for the financial year.

Key points to remember:

- The debt must be unrecoverable

- It must have been previously included in your income

- Documentation must show it was written off before 30 June

Doing this correctly keeps your records accurate and ensures compliance with ATO rules.

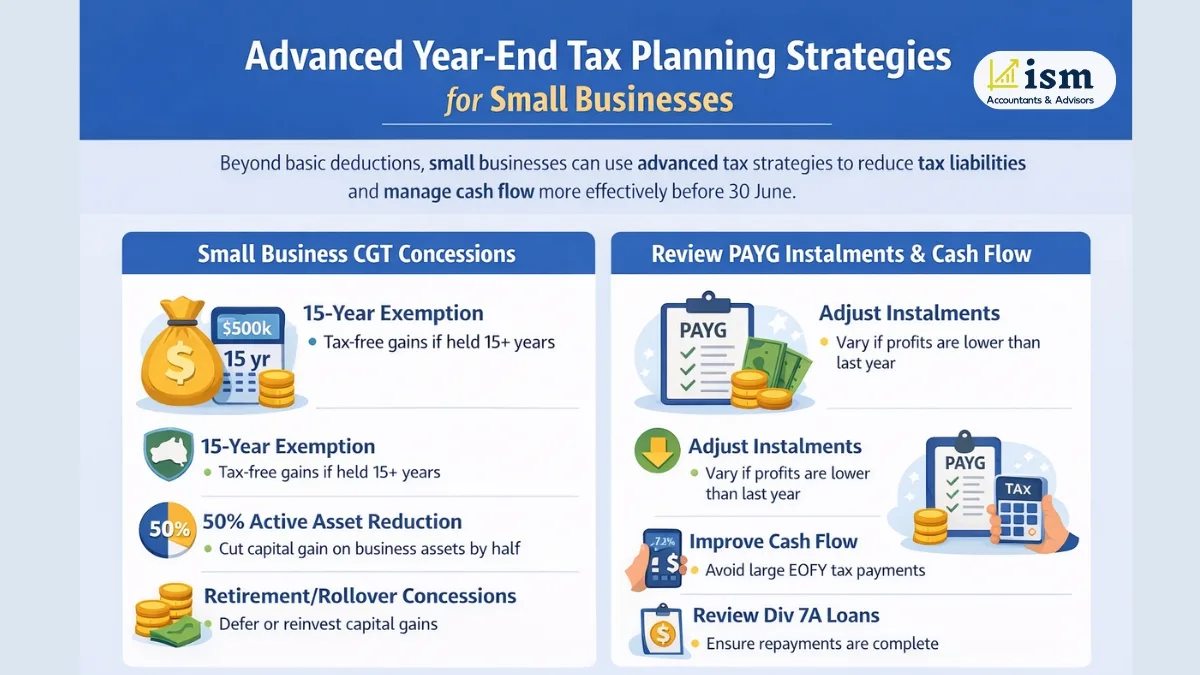

Advanced Year End Tax Planning Strategies

Beyond basic deductions, small businesses can use advanced tax strategies to reduce tax liabilities and manage cash flow more effectively before 30 June. These strategies help optimise end-of-year finances and prepare your business for the new financial year.

7. Small Business CGT Concessions

Small business owners may reduce capital gains tax (CGT) when selling business assets by using available concessions.

Key CGT concessions include:

- 15-year exemption – Exempt from capital gains tax if certain conditions are met

- 50% active asset reduction – Reduces the capital gain on eligible active business assets by half

- Retirement and rollover concessions – Defer or reduce CGT when retiring or reinvesting in other business assets

Applying these concessions strategically can significantly lower your tax liability and increase funds available for reinvestment.

Recommended Read: Payroll Management Strategies

8. Review PAYG Instalments & Cash Flow

Managing PAYG instalments and cash flow helps avoid large end-of-year tax bills and ensures your business stays financially healthy.

Tips for EOFY:

- Vary PAYG instalments if profits are lower than the previous year to match your actual earnings

- Avoid large EOFY tax payments to improve immediate cash flow

- Review Division 7A loans to ensure repayments are completed, preventing unintended dividend declarations

These measures give small businesses better control over finances and help avoid surprises at tax time.

Recommended Read: Single Touch Payroll for Small Businesses

End of Financial Year Deadlines You Should Know (Australia)

Staying on top of key EOFY deadlines is essential for small businesses in Australia. Missing these dates can lead to penalties, missed deductions, or cash flow issues. Planning ahead ensures your business remains compliant with the ATO, maximises deductions, and keeps finances organised.

Date | Task |

March / April | Start reviewing your tax planning and EOFY strategies |

30 June | EOFY planning deadline – complete prepayments, write-offs, and review trading stock |

28 July | BAS lodgement & quarterly super contributions due |

31 October | Tax return lodgement deadline for individuals and businesses |

By keeping track of these dates, small businesses can claim deductions, manage cash flow effectively, and remain compliant with the ATO, avoiding last-minute stress or penalties.

Final Thoughts

End-of-year planning is important for small businesses in Australia. It can help you save tax, keep cash flowing, and stay on top of ATO rules. Acting before 30 June lets you claim deductions, write off bad debts or old stock, manage super contributions, and use incentives like the instant asset write-off and CGT concessions.

Thinking ahead also makes your finances easier to manage in the new year. Keeping track of deadlines, maintaining accurate records, and planning things like PAYG adjustments or timing income can make a noticeable difference.

Being on top of your EOFY tax planning gives your business confidence, clarity, and room to grow, while avoiding penalties or last-minute stress. Contact ISM Accountants for your year end tax planning.

FAQ

The EOFY deadline is 30 June. By this date, you should have finished all your planning, prepayments, write-offs, and checked your deductions so you can make the most of your tax position.

The instant asset write-off lets small businesses claim the full cost of eligible assets under $20,000 right away, as long as the asset is first used or installed by 30 June 2025. If an asset costs more than that, it goes into a depreciation pool and you claim it gradually.

Yes. Small businesses can prepay up to 12 months of expenses like rent, insurance, software subscriptions, or marketing before 30 June to bring those deductions into this financial year.

To get a tax deduction, you can contribute up to $27,500 for 2023–24, and up to $30,000 from 1 July 2024, as long as the contributions reach the super fund before 30 June.

The ATO needs proof that the debt can’t be collected, that it was included as income before, and that it was written off before 30 June. You also need to include any GST adjustments.

Small business CGT concessions can lower or even remove capital gains tax when you sell business assets. Options include the 15-year exemption, 50% active asset reduction, and retirement or rollover concessions.

Yes. If your business uses accrual accounting, you can delay recognising income until after 30 June. This moves taxable income to the next financial year and can lower your tax for the current year.