Buying a car is one of the biggest financial decisions most Australians make, yet it’s also one of the most mishandled, especially when tax is involved. Whether you’re a first-time buyer, a sole trader, or a business owner looking at a tax write-off, the same costly mistakes come up again and again.

At ISM Accountants, we work with clients across Perth who’ve made these errors, and more importantly, we help them avoid them. This guide covers the most critical mistakes buying a car in Australia, with a sharp focus on the tax side that most buyers overlook entirely.

Why Getting the Tax Side Right Matters Before You Buy a Car?

Most buyers walk into a dealership thinking about colour, features, and finance repayments. Very few think about the ATO.

But if you’re buying a car for business use, whether you’re a sole trader, company director, or employee, the tax implications are significant. Get it wrong, and you could miss legitimate deductions, trigger unexpected tax liabilities, or find yourself on the wrong side of an ATO audit.

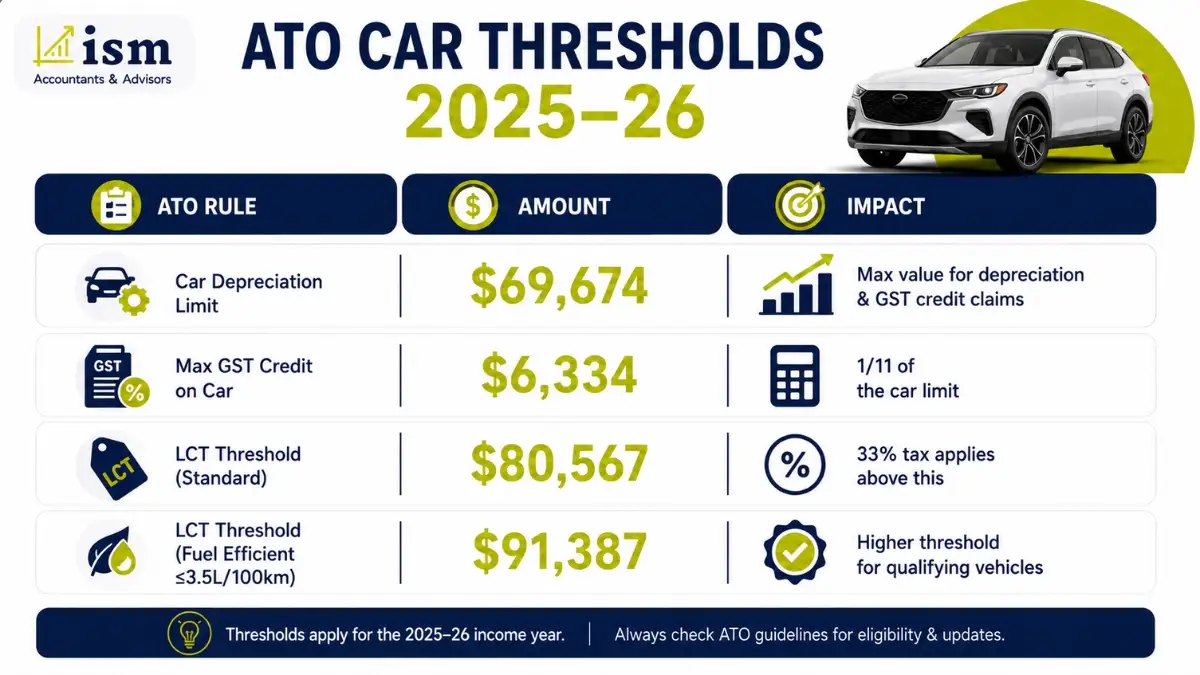

Quick Reference: ATO Car Thresholds 2025–26

ATO Rule | Amount | Impact |

Car Depreciation Limit | $69,674 | Max value for depreciation & GST credit claims |

Max GST Credit on Car | $6,334 | 1/11 of the car limit |

LCT Threshold (Standard) | $80,567 | 33% tax applies above this |

LCT Threshold (Fuel Efficient ≤3.5L/100km) | $91,387 | Higher threshold for qualifying vehicles |

Top 7 Mistakes Buying a Car People Make in Australia

Whether you’re a sole trader tracking a tax deduction or a private buyer hunting for a reliable family ride, you need to know exactly where the traps are hidden.

Here are the seven absolute biggest mistakes people make when buying a car in Australia:

Ignoring the $69,674 ATO Car Depreciation Cap

Getting Blindsided by the 33% Luxury Car Tax

Assuming Business Ownership Equals a 100% Tax Write-Off

Falling for the Weekly Payment Trap

Not Running a PPSR Check on a Private Sale

Not Getting an Independent Inspection Before Purchase

Not Considering the $20,000 Instant Asset Write-Off

Ignoring the $69,674 ATO Car Depreciation Cap

This is one of the most expensive and most overlooked mistakes buying a car in Australia, particularly for business buyers.

The car limit for 2025–26 is $69,674. This is the highest value you can use to calculate depreciation on a car, and the most GST credit you can claim is $6,334, that is, 1/11 of $69,674.

What this means in plain terms: if you buy a $95,000 SUV for your business, you cannot claim depreciation on the full amount. The car limit ATO sets acts as a hard cap. The extra $25,000+ you spent? You can’t depreciate it, and you can’t claim the GST on that portion either.

This catches a lot of sole traders and business owners off guard. They assume claiming a car purchase on tax means claiming the full purchase price. It doesn’t, not unless your vehicle falls under that threshold.

What to do instead: Before signing anything, run the numbers with your accountant. Know exactly what’s deductible and what isn’t, especially if you’re eyeing a vehicle that pushes into luxury territory.

Recommended Read: Tax Deductions in Australia

Getting Blindsided by the 33% Luxury Car Tax

Linked closely to the car limit, the Luxury Car Tax (LCT) is another major mistake buying a car that business buyers don’t see coming.

LCT is payable at 33% of the GST-inclusive value that exceeds the LCT threshold. As of 2024, the LCT threshold is $80,567. An increased threshold of $91,387 applies to fuel-efficient cars with a combined fuel consumption rating not exceeding 3.5 litres per 100km as of 1 July 2025.

So if you’re purchasing a vehicle for $90,000, you’re already paying LCT on roughly $9,000+ of that value, at 33%. That’s an extra cost that gets baked into the purchase price, and in most cases, it’s not directly tax-deductible for businesses.

What’s changed recently: From 1 July 2025, the definition of a fuel-efficient vehicle changed, meaning a car only qualifies for the higher LCT threshold if it has a fuel consumption that does not exceed 3.5 litres per 100km, previously this was 7 litres per 100km. Many hybrid vehicles that previously enjoyed the higher threshold no longer qualify.

If you were planning to claim a car on tax Australia and assumed your hybrid SUV would qualify for the fuel-efficient threshold, check again. This change catches a lot of buyers in 2025–26.

Assuming Business Ownership Equals a 100% Tax Write-Of

One of the most common misconceptions around buying a car for business tax write-off in Australia is assuming that simply putting a car under a business name makes it 100% deductible. That’s not how it works.

The ATO requires you to substantiate the actual percentage of business use. If you use your car 60% for business and 40% for personal use, you can only claim 60% of eligible expenses. That includes fuel, insurance, registration, maintenance, and depreciation up to the car depreciation limit 2026 ($69,674 for 2025–26).

For sole traders especially, this is critical. A sole trader car tax write-off Australia is legitimate and valuable, but only when properly documented. The ATO accepts two methods:

- Logbook method: Keep a logbook for 12 continuous weeks to establish your business-use percentage, then apply it to all car expenses for the year.

- Cents per kilometre method: Claim a flat rate per kilometre (currently 88 cents/km) for up to 5,000 business kilometres per year. No logbook required, but no depreciation claim available under this method.

Not keeping records is one of the biggest ATO car tax deduction warnings we give clients. If you’re audited and can’t substantiate your claim, those deductions get reversed, with interest and penalties on top.

Recommended Read: Bookkeeping Practices for New Entrepreneurs

Falling for the Weekly Payment Trap

This is a classic dealership tactic that has nothing to do with tax, but everything to do with costing you thousands.

A dealership finance manager will quote you something like “it’s only $145 a week.” That sounds manageable. But break it down: $145 a week over 7 years is over $52,700 in repayments, before you even factor in interest. On a car that might depreciate to $18,000 in that time.

Longer loan terms (72, 84, or 96 months) create extended periods of negative equity, meaning you owe more than the car is worth for most of the loan term. If you’re trying to use that vehicle as a business asset and claim depreciation, the mismatch between what you owe and the car’s book value creates a financial mess.

The smarter approach: Get pre-approved finance through a bank, credit union, or independent finance broker before you step into a dealership. You’ll negotiate on the total price, not the weekly figure, and avoid paying thousands in unnecessary interest.

Not Running a PPSR Check on a Private Sale

If you’re buying privately, this one can cost you the entire price of the car. The Personal Property Securities Register (PPSR) check is a $2 government search that tells you whether the vehicle has money owing on it, has been written off, or has been reported stolen.

Skip this check and buy a car with finance still attached, and the lender can legally repossess it from you, even if you paid in good faith. You’d lose the car and the money with virtually no recourse.

Given that this mistake buying a car privately costs just $2 to avoid, there’s genuinely no excuse to skip it.

Not Getting an Independent Inspection Before Purchase

Whether buying privately or from a dealer, relying solely on a “look-over” or the seller’s word is a significant error. State motoring bodies like the NRMA, RACV, or RACQ offer independent pre-purchase inspections that identify structural damage, mechanical faults, and safety issues that aren’t visible to the untrained eye.

This matters doubly for business buyers. A vehicle with hidden mechanical issues that fails six months in isn’t just an inconvenience, it interrupts business operations, creates unplanned expenses, and if it’s your depreciating business asset, those repair costs add complexity to your tax position.

Not Considering the $20,000 Instant Asset Write-Off (Where Eligible)

The instant asset write-off has had a complicated history in Australia, with thresholds changing regularly. For the 2024–25 income year, eligible small businesses (with a turnover under $10 million) could immediately deduct the full cost of eligible depreciating assets under $20,000, rather than writing them off over several years.

This does not typically apply to cars exceeding the car limit ATO threshold ($69,674). However, for business vehicles like vans, Utes with a payload over one ton, or commercial vehicles that fall outside the passenger vehicle definition, different rules may apply and the full cost may be immediately deductible.

This is where speaking to an accountant before, not after, you buy is genuinely worth money. Choosing the right vehicle type, structured the right way, at the right time of year, can make a material difference to your tax position.

If it’s a standard passenger car costing more than $20,000, you cannot write it off instantly. You must claim it over several years. However, if you buy a commercial vehicle (like a dual-cab Ute with a carrying capacity over 1 tonne), different rules apply.

Recommended Read: How to Manage Business Debt and Improve Financial Health in Australia?

What's the Most Tax-Effective Way to Buy a Car in Australia?

There’s no single answer, it depends on your structure, income level, and how much the vehicle will genuinely be used for business. But broadly:

- Sole traders and individuals: Logbook method gives the most flexibility and the highest deductions when business use is high. Claim car purchase on tax through your individual tax return.

- Companies and trusts: The car is owned by the entity, and all legitimate business expenses (including depreciation to the car limit ATO) are deductible against income.

- Employees with novated leases: Pre-tax dollars fund the vehicle through salary packaging, which can be effective, but FBT implications need to be carefully assessed.

- FBT-exempt EVs: Electric vehicles under the LCT threshold (currently $91,387 for fuel-efficient vehicles) may be eligible for FBT exemption on novated leases, a significant benefit worth exploring in 2026.

Final Thoughts

The mistakes buying a car in Australia that cost people the most money aren’t always about choosing the wrong model or paying too much at the dealership. Increasingly, the biggest losses happen on the tax and finance side, buying a car for business tax write-off Australia without understanding the ATO’s rules, missing the car depreciation limit 2026, or locking into a long-term loan that makes no financial sense.

The good news: all of these are avoidable with the right advice before you buy, not after.

At ISM Accountants, we help individuals, sole traders, and business owners in Perth navigate exactly these decisions. Whether you’re weighing up the tax impact of a vehicle purchase, need help with your logbook and records, or want clarity on what you can actually claim, we’re here to help. Contact us today.

Call us on 08 6333 0375

Email: info@ismaccountants.com.au

2 Mint St, East Victoria Park WA 6101

FAQ: Mistakes Buying a Car in Australia

Can you claim buying a car on your taxes in Australia?

Yes, but only if the vehicle is used for income-producing or business purposes. You can claim a deduction for the business-use portion of running costs and depreciation, up to the ATO car limit of $69,674 for 2025–26. You cannot claim the full cost of a personal vehicle.

What is the car depreciation limit for 2026?

The ATO car limit for the 2025–26 financial year is $69,674. This is the maximum value you can use to calculate depreciation deductions on a passenger vehicle, regardless of what you paid for it.

What is the most tax-effective way to buy a car in Australia?

It depends on your structure. For sole traders and individuals, the logbook method maximises deductions when business use is high. For businesses, owning through a company and claiming depreciation up to the ATO car limit is common. Novated leases work well for employees. An accountant can identify the right structure for your specific situation.

How does the $20,000 instant asset write-off work?

Eligible small businesses (turnover under $10M) can immediately deduct the full cost of assets under $20,000 in the year they’re purchased. Standard passenger cars rarely qualify at that price point, but commercial vehicles outside the passenger vehicle definition may. Always confirm eligibility with your accountant before purchase.

What is the Luxury Car Tax threshold in Australia for 2025–26?

The LCT threshold is $80,567 for standard vehicles. Fuel-efficient vehicles (under 3.5L/100km from 1 July 2025) have a higher threshold of $91,387. LCT is charged at 33% on the value above these thresholds.

What is the biggest mistake first-time car buyers make?

Beyond emotion-driven decisions, the most costly mistake is not accounting for the true on-road cost, stamp duty, registration, insurance, CTP, and in the case of business buyers, not understanding what they can and can’t claim on tax before committing to a purchase.

What is a sole trader car tax write-off in Australia?

Sole traders can claim car expenses for vehicles used in their business using either the logbook method or the cents-per-kilometre method. Under the logbook method, you can claim depreciation up to the car limit ATO, plus eligible running costs proportional to business use. Accurate records are essential.

Is the PPSR check really necessary?

Absolutely. It’s a $2 government check that protects you from buying a car that has money owing on it, has been written off, or is stolen. Skipping it in a private sale can result in losing both the car and your money.

This article is for general informational purposes only and does not constitute formal tax advice. Please consult a registered tax agent for advice specific to your circumstances.